Yet Another Proxy for Immiseration

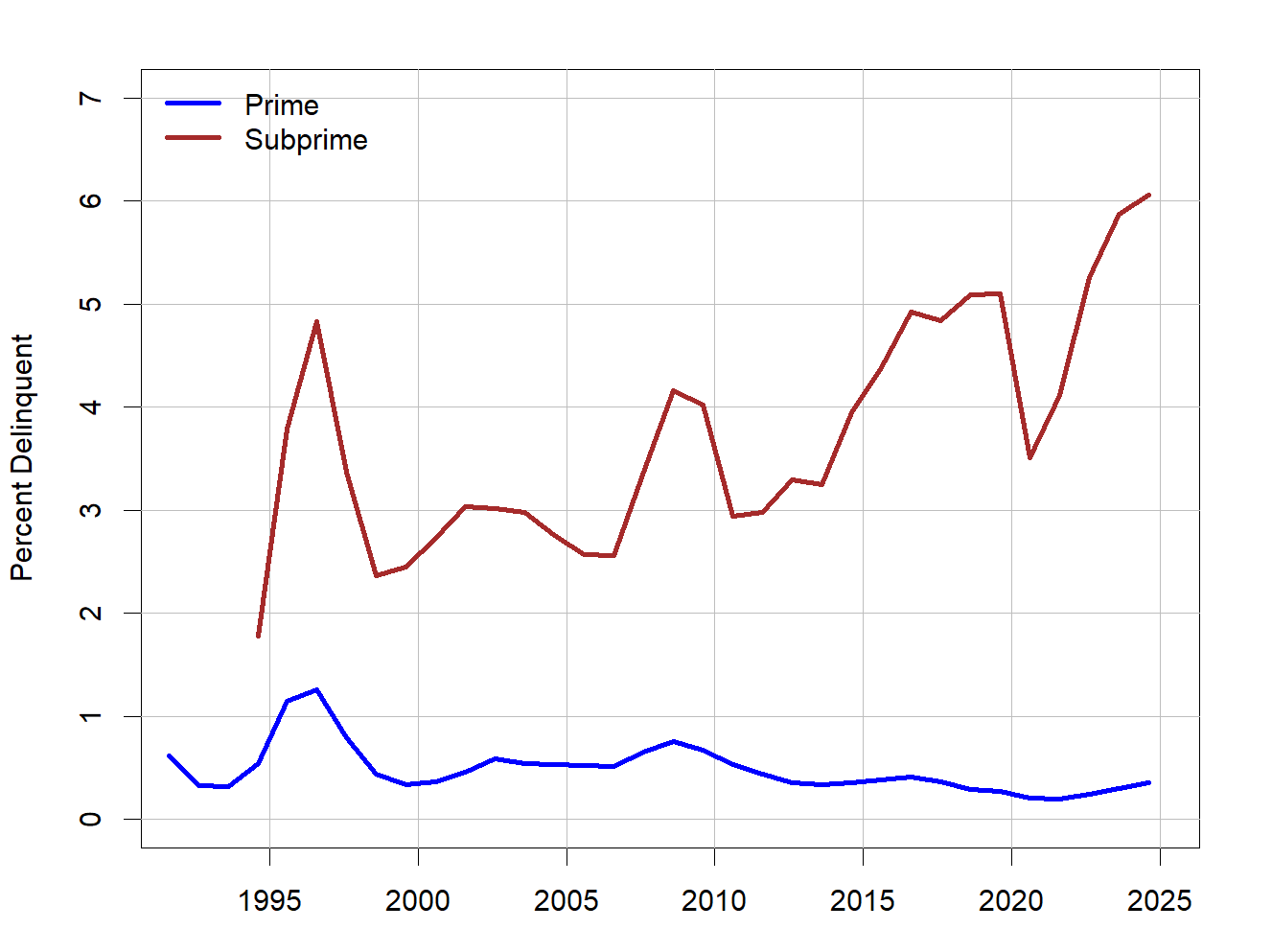

Car loan delinquency rate

I am working on the next installment in the series on the Structural-Demographic State of America. It will deal with trends in well-being (and, alternatively, immiseration) and will be published Friday. In the meantime I saw a new dataset for an immiseration proxy. I haven’t used it before, but it tells an interesting story; worth a short post.

The data is from Fitch Ratings on the US auto loan delinquency index, which tracks the proportion of car loans where payments are 60 days or longer past due. The index tracks separately customers with good credit rating (prime) and those with poor credit (subprime).

Because I am interested in the long-term trends, I annualized the monthly data from Fitch Ratings (by averaging over 12-month periods). And here’s the result:

There are two interesting features here. First, borrowers with poor credit, which usually means the poor, are increasingly unable to keep up with car payments. Second, there are substantial fluctuations around the trend, with peaks roughly corresponding to recessions in the United States (except for the 1996-7 peak, which was due to an auto credit bubble correction). What is interesting is that initially peaks in the prime sector paralleled those in the subprime sector, but with time these prime fluctuations smoothed out. I am not entirely sure why this happened, but one possible explanation is that the economic conditions for these two sectors have increasingly diverged since 2000.

In any case, these data are yet another confirmation of increasing economic inequality in the US and the immiseration of lower-income Americans. Some of you, readers, may say “well, it’s obvious!” But my experience shows that there is never too much data.

Having been in the used car biz, I can attest that it's good for a lot of useful data. Prime vs subprime defaults; auction action, indicating the financial health of the dealers; and the overall prices of inventory as a reflection of general demand, for example.

From my limited understanding of the car market, dealers prefer selling through finance rather than to cash buyers because of the additional fees they receive. Follow the incentives, and you can see why dealerships are bending over backwards to shoehorn less creditworthy buyers into finance deals — they’re not the ones on the hook when those loans go bad.

It’s basically the same setup that fuelled the subprime mortgage fiasco.